In my book ‘How To Manage Your Money Like The Rich and Famous’ I avoided mentioning any financial products by name. The reason is because I want my readers to research and build an LPD financial strategy genuinely suited to their own needs, location, and financial regime. I don’t sell products, or gimmicks – my aim is to help smaller investors create genuine financial strategies which help stabilise their finances through the uncertainties of life.

In my blog, by contrast, I will mention products and financial companies by name, but only because I want to use them to illustrate general principles. While I may be using these products myself, I want to make clear I am not endorsing them for anyone else to use. Your situation, your finances, your location, your tax regime, will demand different product solutions. Your financial strategy will be different to mine, because your life and needs are different. I intend to be brutally honest in these blogs, because our most valuable financial lessons are learned from our mistakes.

Let me be clear: I do not take commission or affiliate income from any products or companies. Don’t take short cuts by copying what I do – do your own research, build your own financial strategy, stabilise your own finances, secure your own life.

The great thing about having built a genuinely tailored financial strategy, using LPD principles, is it’s flexible. You know why you invested this here, that there, what you might be saving for, what individual financial risks need mitigating. So, when the world changes, you can adapt your financial strategy accordingly.

Living in the UK, I am constrained by UK financial and tax regimes as to where I can invest. When the UK was part of the European Union, I also had access to a wider range of products offered by EU countries. Over the past year, given the uncertainties of the UK/EU future relations, I have withdrawn my money from all EU products and companies. That money was reinvested in the UK.

In your own locations and countries, you will face localised constraints on your investments, but you will also have opportunities to which I have no access.

When times are uncertain, the general rule is to contract and give yourself easier access to your money. This depends mainly, of course, on what happens to your income. In the Covid crisis, if your income has become less certain, or disappeared completely, you will need to draw on what you have already saved and invested, while you stabilise or replace your income.

If you were saving for ‘a rainy day’, it may now be pouring in your life. – if that is your experience, I feel for you, and hope my book may have made some small tangible difference to your finances.

Some financial adjustment has been required to my own financial strategy:

Funding Circle, the Peer-to-Peer small business loan platform, shut its doors to new retail customers at the start of the crisis. Instead they concentrated on lending out government recovery money – great for small business, not so good for retail investors like me. From my perspective, any platform that cannot keep 100% of my money invested, is ‘toast’. I immediately tried to cash in my whole investment, intending to redivert it to Exchange Traded Funds (ETF) during the market crash – more about ETF’s later.

However, Funding Circle, no doubt anticipating the reaction of its retail customers, also closed its secondary market. Making it impossible for me to uninvest my money. Whether Funding Circle will ever open again to retail investors is anybody’s guess. In the mean-time, every month I withdraw any interest paid and any moneys repaid from loans. I reckon in the medium term, I may recover 80% of my investment in Funding Circle, with the rest following in the long term. Whilst the risk of losing all my money from Funding Circle is low, I have potentially lost out by not being able to take advantage of market volatility through ETFs.

Assetz Capital (Peer-to-Peer mixed loans) has remained open to retail investors, but they have tightened their credit criteria for new loans – which is exactly what I would want to happen. Most of my investments there are in 30-day accounts, which invest in a variety of personal loans and short-term business loans. Defaults have increased a bit, but overall interest is only down by 1%, which is within their projected performance criteria. So, my money remains invested where it is.

My other investments with Assetz Capital are in their manual secondary market. I use this to boost my overall interest by taking on a small number of higher risk/high interest loans, mostly in the commercial property market. This is an area that may be heavily impacted in the future by the Covid crisis, as more people work from home. There is nothing I can do about my existing commercial loans, though as the volume I hold is low, the overall risk to my wider investments is also low. I have instead switched to manually investing in short term bridging and development loans – the interest is still high, but the turn-around is much quicker, which decreases the long-term risk.

Zopa (Peer-to-Peer personal loans) has also tightened its lending criteria. Personal loan defaults have increased a bit, but also Zopa has offered ‘payment holidays’ to its clients. Whilst this may reduce the overall default rate of loans, it may also mean pushing the problem into the future. Currently, my interest returns are down about 1% at Zopa. Again, this is within their projected criteria, so my investment remains in place.

My Exchange Traded Fund (ETF) investments have performed surprisingly well through the Covid crisis. Yes, they crashed when the rest of the world economy crashed, but they have come back quite strong and are currently on a par with where they were before the crash.

As I said above, my grand plan was to use money withdrawn from Funding Circle to invest in new ETFs while the markets were in shock. That plan was resoundingly scuppered by Funding Circle. So, as the returning money from Funding Circle builds in my savings account, I am looking for new long-term opportunities in ETFs.

I am tempted by ETFs in the technology sectors, which have performed well during the crisis. Also, the Pharmaceutical sector would appear to be an obvious opportunity in the short to medium term. Which pharmaceutical companies will ultimately triumph with a Covid-19 vaccine are impossible to predict. To this end, I would only invest in funds which track a pharmaceutical index. By automatically self-correcting, ditching bad performers and replacing them with better performers, a tracker fund will mitigate any element of gambling.

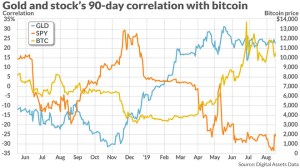

Bitcoin has also remained remarkably stable throughout the crisis, a surprise to most, as has gold. I feel the main opportunity for gold has now passed, but technologies which invest in crypto currencies, might well provide future opportunities in the medium to long term. As you will know from my book ‘How To Manage Your Money Like The Rich And Famous’ our LPD principles favour the stability of investing in ‘shovels’ rather than prospecting for ‘gold’.

Investing in an uncertain world, as the nature of the financial risks we face change, requires flexibility, agility, and rebalancing. However, a well-researched individual financial strategy, built on LPD principles, will be up to the challenge.

Wishing you well with your finances,

Nick